Sunday, January 5, 2020

Market Mogul articles available on TN Economics blog

Hi all! Sorry for the inactivity on the page. Unfortunately, The Market Mogul has officially rebranded into Mogul News, and have deleted all content on the previous website, including the articles I have published before. Thankfully, we will be posting them onto the blog, and hopefully new content again on the website! Thank you for everything and happy reading!

Monday, January 21, 2019

A Shares and H Shares – Why Can The Same Company's Shares Have Different Prices? [Published March 2018]

Not all stock markets are created equal. Every country’s stock market has its own distinct set of listing requirements, trading rules, securities governing entity, the degree of technological advancement and composition of investor types (retail and institutional) to name a few.

For instance, less developed stock exchanges may have lower listing requirements relative to a more developed market to attract domestic businesses to list at home rather than abroad as well as foreign capital.

Companies can choose to list at home, abroad or both depending on the management’s view on the best course of action. In the years post-financial crisis, the NASDAQ has won several big IPOs from domestic and foreign technology firms such as Facebook (2012), Alibaba (2014) and more recently Snap (2017) because it offered Weighted Voting Rights (WVR) for founders that want to have greater control over the company they built from the ground up, influencing its long-term goals and direction.

This was the primary reason why Alibaba refused to list on the Hong Kong Exchange since they did not offer WVRs, sticking to an outdated “one share, one vote” system.

These differences account for the different valuations and market sentiment toward the country’s market. But what about the price of shares of a company? In theory, the stock price of a company that is listed on different exchanges should be equal after converting into common currency because the share price performance is based on the group’s consolidated financial statements from its operations globally. If so, the share price reflects all publicly available information regardless of which exchange the stock is listed on. In this case, there should be no need to distinguish between fundamental or technical trading.

This theory somewhat holds true to some extent. The share prices of the same company are roughly similar after accounting for exchange rates. Small differences exist but are treated as negligible. Furthermore, they exhibit very similar patterns and movements at varying levels of volatility. One example is Rio Tinto, the Australian-British metals and mining company. It is listed on both the London Stock Exchange and the New York stock exchange as the same entity. After converting into common currency based on the end-of-day exchange rate, there is a small difference of 1 to 2 dollars, but these small differences may be attributed to the imperfect markets.

Where the theory does not apply well is when one looks at the share price of companies in the Hong Kong and Mainland China stock exchanges. Chinese companies often choose to list in Hong Kong as opposed to the Mainland because Hong Kong’s stock exchange market is more developed, has a large foreign investor population, offers a better legal environment and functions as close to a laissez-faire economy as anywhere in the world.

For the Chinese companies listed in both Hong Kong and either Shanghai or Shenzhen, investors classify those shares as H-shares and A-shares respectively. The number of H-share companies is equal to 248 (Main Board = 224, Growth Enterprise Market = 24), and thus there is an equivalent number of A-shares.

Below is a graph of the Hang Seng AH Premium index which tracks the average price difference of A-shares over H-shares for the largest and most liquid Chinese companies:

(Source: FT)

If there was no price difference between A-shares and H-shares, then the index would be at 100. Over the last five years, particularly in between 2012 and the end of 2014, the index has fluctuated between 90 to 115. Although there was volatility, the index alternating between premium and discount suggests these price differences are mostly systematic.

Over the past three years, however, the AH premium index has consistently been above 100, currently hovering around 120 which indicates A-shares are at a 20% premium to H-shares. Interestingly, the AH premium jumped 30 points after the introduction of the Shanghai-HK (“SH-HK”) stock connect program in late 2014. The Shenzhen-HK (“SZ-HK”) stock connect, launched in late 2016, has had almost no effect.

The Stock Connect programs should have narrowed the premium or discount because it allowed foreign investors to buy A-shares and other Mainland-listed stocks through the Hong Kong exchange, so investors do not have to purchase H-shares just to gain exposure to that company. If there were any price differences, investors may identify that as an arbitrage opportunity and swiftly eliminate the price difference.

There have been several studies that aim to understand this phenomenon. One study by Tingting Wu and Xiaoying Gao titled “Factors of Price Difference between A-Shares and H-Shares under SH-HK Stock Connect“, identified four important factors:

Asymmetric Information – There are two sides to this argument. On the one hand, Mainland companies register and operate in China, where certain factors such as geography, culture, and differences in regulation may affect H-Share investors from accessing information. On the other hand, the H-Shares market may contain more information due to closing behind the A-Shares market. For an A-H dual-listed company for = 1, 2, … , the combined total market capitalization expressed in renminbi is used as a proxy for asymmetric information. It is predicted that a larger combined total market capitalization would reduce asymmetric information and therefore narrow the AH price difference.

The study runs a panel data regression model to test the above factors’ relationship with and significance against the A-H price ratio. The results confirm all but the differential risk preference hypothesis; This makes sense because the Stock Connect programs have diversified the investor pool investing in A-Shares, whom bring their experience from overseas markets to China and extending the investment time horizon.

The paper concludes with straightforward policy recommendations, for example, making A-Share investors more educated, speeding up financial innovation to establish effective arbitrage mechanisms, and launch the SZ-HK Stock Connect (already in place by the time of writing).

When will the price difference be eliminated? It is difficult to envision when this may happen, but it will be highly dependent on initiatives to further reduce capital flow frictions, improve information systems for transparency, and open more investment channels to Mainland investors for a more level playing field. Because no two stock markets are equal, their respective market properties can affect stock valuation.

Although China’s economy has become more open from its past communist regime, it is nowhere near to the economic freedom enjoyed in Hong Kong. The government’s helping hand has turned China into an economic superpower. To continue reaping the benefits of globalization, it should strive to make itself the global choice for equity investors.

For instance, less developed stock exchanges may have lower listing requirements relative to a more developed market to attract domestic businesses to list at home rather than abroad as well as foreign capital.

Companies can choose to list at home, abroad or both depending on the management’s view on the best course of action. In the years post-financial crisis, the NASDAQ has won several big IPOs from domestic and foreign technology firms such as Facebook (2012), Alibaba (2014) and more recently Snap (2017) because it offered Weighted Voting Rights (WVR) for founders that want to have greater control over the company they built from the ground up, influencing its long-term goals and direction.

This was the primary reason why Alibaba refused to list on the Hong Kong Exchange since they did not offer WVRs, sticking to an outdated “one share, one vote” system.

Theory of Same Stock Price Equality

These differences account for the different valuations and market sentiment toward the country’s market. But what about the price of shares of a company? In theory, the stock price of a company that is listed on different exchanges should be equal after converting into common currency because the share price performance is based on the group’s consolidated financial statements from its operations globally. If so, the share price reflects all publicly available information regardless of which exchange the stock is listed on. In this case, there should be no need to distinguish between fundamental or technical trading.

This theory somewhat holds true to some extent. The share prices of the same company are roughly similar after accounting for exchange rates. Small differences exist but are treated as negligible. Furthermore, they exhibit very similar patterns and movements at varying levels of volatility. One example is Rio Tinto, the Australian-British metals and mining company. It is listed on both the London Stock Exchange and the New York stock exchange as the same entity. After converting into common currency based on the end-of-day exchange rate, there is a small difference of 1 to 2 dollars, but these small differences may be attributed to the imperfect markets.

AH Share Premium

Where the theory does not apply well is when one looks at the share price of companies in the Hong Kong and Mainland China stock exchanges. Chinese companies often choose to list in Hong Kong as opposed to the Mainland because Hong Kong’s stock exchange market is more developed, has a large foreign investor population, offers a better legal environment and functions as close to a laissez-faire economy as anywhere in the world.

For the Chinese companies listed in both Hong Kong and either Shanghai or Shenzhen, investors classify those shares as H-shares and A-shares respectively. The number of H-share companies is equal to 248 (Main Board = 224, Growth Enterprise Market = 24), and thus there is an equivalent number of A-shares.

Below is a graph of the Hang Seng AH Premium index which tracks the average price difference of A-shares over H-shares for the largest and most liquid Chinese companies:

(Source: FT)

If there was no price difference between A-shares and H-shares, then the index would be at 100. Over the last five years, particularly in between 2012 and the end of 2014, the index has fluctuated between 90 to 115. Although there was volatility, the index alternating between premium and discount suggests these price differences are mostly systematic.

Over the past three years, however, the AH premium index has consistently been above 100, currently hovering around 120 which indicates A-shares are at a 20% premium to H-shares. Interestingly, the AH premium jumped 30 points after the introduction of the Shanghai-HK (“SH-HK”) stock connect program in late 2014. The Shenzhen-HK (“SZ-HK”) stock connect, launched in late 2016, has had almost no effect.

The Stock Connect programs should have narrowed the premium or discount because it allowed foreign investors to buy A-shares and other Mainland-listed stocks through the Hong Kong exchange, so investors do not have to purchase H-shares just to gain exposure to that company. If there were any price differences, investors may identify that as an arbitrage opportunity and swiftly eliminate the price difference.

Factors from Empirical Studies

There have been several studies that aim to understand this phenomenon. One study by Tingting Wu and Xiaoying Gao titled “Factors of Price Difference between A-Shares and H-Shares under SH-HK Stock Connect“, identified four important factors:

Asymmetric Information – There are two sides to this argument. On the one hand, Mainland companies register and operate in China, where certain factors such as geography, culture, and differences in regulation may affect H-Share investors from accessing information. On the other hand, the H-Shares market may contain more information due to closing behind the A-Shares market. For an A-H dual-listed company for = 1, 2, … , the combined total market capitalization expressed in renminbi is used as a proxy for asymmetric information. It is predicted that a larger combined total market capitalization would reduce asymmetric information and therefore narrow the AH price difference.

- Liquidity – The A-Share market is assumed to have greater liquidity than the H-Share market because of the large retail investor population in China and A-Shares being the first choice of equity investments due to narrow investment channels. The turnover of H-Shares over A-Shares is used as the proxy for liquidity. It is predicted that an increase in liquidity of H-Shares would reduce the AH premium.

- Differential Demand Elasticity – Hong Kong investors have many investment channels, but A-Shares are almost the only choice for Mainland investors. Furthermore, while Hong Kong and overseas investors can trade Mainland-listed securities without restrictions, Mainland investors can only trade if their accounts hold an aggregate balance of RMB 500,000 in cash and/or securities. Not many people can satisfy this criterion, so it creates a situation where they can only invest in A-Shares. The proportion of H-Shares in total outstanding shares is used to express elasticity of demand; greater elasticity is expected to reduce the AH premium.

- Differential Risk Preference – The paper distinguishes A-Share and H-Share investors by their investment-horizon; A-Share investors focus on short-term profits from speculation, and H-Share investors focus on long-term returns and dividends. It is a reasonable explanation for the inherent volatility in Mainland markets, remember the 2015 Shanghai stock market crash, anyone?

The study runs a panel data regression model to test the above factors’ relationship with and significance against the A-H price ratio. The results confirm all but the differential risk preference hypothesis; This makes sense because the Stock Connect programs have diversified the investor pool investing in A-Shares, whom bring their experience from overseas markets to China and extending the investment time horizon.

The paper concludes with straightforward policy recommendations, for example, making A-Share investors more educated, speeding up financial innovation to establish effective arbitrage mechanisms, and launch the SZ-HK Stock Connect (already in place by the time of writing).

Fundamental Differences

When will the price difference be eliminated? It is difficult to envision when this may happen, but it will be highly dependent on initiatives to further reduce capital flow frictions, improve information systems for transparency, and open more investment channels to Mainland investors for a more level playing field. Because no two stock markets are equal, their respective market properties can affect stock valuation.

Although China’s economy has become more open from its past communist regime, it is nowhere near to the economic freedom enjoyed in Hong Kong. The government’s helping hand has turned China into an economic superpower. To continue reaping the benefits of globalization, it should strive to make itself the global choice for equity investors.

Thursday, January 17, 2019

Hong Kong Stock Exchange's Path to Modernization

Hong Kong has established itself as one of the top IPO venues in the world. According to the World Federation of Exchanges, the Hong Kong Stock Exchange ranked no.1 five times in the last 8 years (2009, 2010, 2011, 2015 and 2016). This is due to its simple tax system, established professional services industries, common law system and proximity to the mainland.

In the last five years, improving market integration with and giving foreign investors access to mainland companies have been Hong Kong’s core strategy. In 2012 and 2014, equity trading links to the mainland were set up through the stock connect programs to Shanghai and Shenzhen respectively. On July 3 this year, the China-Hong Kong Bond Connect program began, giving offshore investors another way to access the mainland’s $10trn market.

More recently on June 27, more than $6.1bn was wiped out from the Small-Cap stocks after the “Enigma Network” report from former HKEX board member and activist investor David Webb riled the Hong Kong market; 17 companies had lost more than 40% of their value, among them was China Jicheng and Greater China Professional Services both of whom sank more than 90%.

These recent market routs have investors and policymakers questioning the integrity of the market, whether there are more problematic companies waiting to be uncovered by the next short seller, and whether this may discourage prospective companies from listing in Hong Kong.

Shrinking Significance?

The growing influence and competency of the mainland has everyone contemplating whether they should eventually stop relying on Hong Kong’s platform to connect with international investors. In 1997, Hong Kong accounted for 16% of China’s total GDP, this number is only 3% today.

Another problem with Hong Kong’s market is its industry composition. The HKEX Main Boardis rooted in the ‘old’ economy that although has served the economy well, is extremely susceptible to external shocks and cyclical movements in the economy. Financial, and Property and Construction companies make up 44% of the Hong Kong stock exchanges’ total market capitalization, whereas only 10.2% is from IT companies as of the end of 2016.

While IT’s share of the market has increased from 3.76% in 2012 to its current level (14.3% YOY increase), it is still underrepresented compared to other major financial centres. For example, the market capitalization weighting and composition for the New York Stock Exchange (NYSE) is more balanced. Financial and Real Estate account for 35.9%, while Information Technology accounts for 33% of the S&P 500’s total market capitalization.

To address these problems, the Hong Kong Exchanges and Clearing (HKEX) issued two new concept papers last month. The first paper outlines plans to overhaul the current Growth Enterprise Market board (GEM) listing requirements, and second paper details a proposal of the “New Board” to attract “New Economy” companies.

However, the current rules which allow these small, loosely regulated companies to list on GEM have created an environment where such problematic companies flourish. The NYSE, for example, says that companies trading at less than $1 per share (penny stocks) will face delisting after 30 consecutive days. HKEX has no such rules in place.

When 40% of the roughly 2000 common stocks traded is less than HK$1 per share, accounting for 4% of the total market capitalization of the exchange, it highlights the structural flaws created by GEM. New listings on GEM are only required to offer a minimum 25% of total shares to a minimum of 100 shareholders.

Since senior management is likely to keep the lion’s share for themselves, this creates a low liquidity, high volatility environment resulting from a high concentration of public shares in few shareholders. The potential big moves have attracted the attention of short sellers to descend on GEM-listed companies. In the recent stock rout, 7 of the 20 biggest decliners were listed on the GEM. The top three decliners were GEM companies: Luen Wong Group (-89%), Greater China Professional (-94%) and China Jicheng Holdings Ltd. (-95%).

Both the Main Board and GEM require that the company must be profitable to be considered for listing. Many of the “New Economy” sectors are unable to reach profitability due to factors including aggressive growth strategy and upfront research and development (R&D) costs. For example, biotech and healthcare tech companies have extremely high R&D costs, and would likely not be profitable until the product becomes commercially viable. HKEX seeks to address this missing market with the New board.

New board PRO companies need to have HK$200m minimum market capitalization and are only open to professional investors but do not require prior financial track record. Meanwhile, New Board PREMIUM companies need to have equivalent listing requirements as Main Board companies (minimum HK$500m market cap and public float of HK$125m) but are open to both retail and professional investors.

Furthermore, the New Boards would for the first time allow a weighted voting rights (WVR) structure which could make a listing in Hong Kong more attractive because it gives greater voting rights to founders, thus protect their vision for the company.

HKEX have explored the inclusion of WVR structures for SMEs in the GEM exchange back in 2014, after losing out on Alibaba’s IPO to NYSE because the HKEX refused to allow senior executives to nominate its board. However, the proposal was ultimately put on hold after mixed responses from over 200 respondents which consisted of large corporations, government and independent organisations. On the one hand, the ones who voted against WVR state that the structure violates the ‘one share, one vote’ principle of the HKEX.

On the other hand, the ones who voted for WVRs believed that it is applicable in certain circumstances, and the simplistic ‘one share, one vote’ principle can lead to short-termism in the absence of a controlling shareholder. No matter which side of the argument is correct, it is undeniable that Hong Kong’s loss is New York’s win. Alibaba went on to record the biggest ever IPO, raising over $25bn. Other developed markets have a similar, more flexible system in place for high tech, intangible asset-heavy companies.

For example, Snap Inc. has never made positive operating cash flow or profit, but still,manages to list on NYSE and was valued at US$25bn in this year’s hottest tech IPO. Co-Founders Evan Spiegel and Bobby Murphy hold a combined 88.5% of the voting power as a result of the triple-class WVR structure, giving them uncontested decision-making authority.

If HKEX does not take steps to keep up or go beyond the competition, they could get left behind in the modern financial system. The revisions to GEM could mitigate the issues resulting from the small public float, while the New Board can attract local “New Economy” sectors to consider Hong Kong over New York. Whether these changes will be effective or not, it is a step in the right direction.

In the last five years, improving market integration with and giving foreign investors access to mainland companies have been Hong Kong’s core strategy. In 2012 and 2014, equity trading links to the mainland were set up through the stock connect programs to Shanghai and Shenzhen respectively. On July 3 this year, the China-Hong Kong Bond Connect program began, giving offshore investors another way to access the mainland’s $10trn market.

Not All Rosy

However, Hong Kong has every right to be worried about its future importance to the Asian financial markets. The Hong Kong stock exchange has seen some wild erroneous moves this year. Huishan Dairy Holdings declined 85% on March 24 after becoming a target of activist short seller Carson Block from Muddy Waters.More recently on June 27, more than $6.1bn was wiped out from the Small-Cap stocks after the “Enigma Network” report from former HKEX board member and activist investor David Webb riled the Hong Kong market; 17 companies had lost more than 40% of their value, among them was China Jicheng and Greater China Professional Services both of whom sank more than 90%.

These recent market routs have investors and policymakers questioning the integrity of the market, whether there are more problematic companies waiting to be uncovered by the next short seller, and whether this may discourage prospective companies from listing in Hong Kong.

Shrinking Significance?

The growing influence and competency of the mainland has everyone contemplating whether they should eventually stop relying on Hong Kong’s platform to connect with international investors. In 1997, Hong Kong accounted for 16% of China’s total GDP, this number is only 3% today.

Another problem with Hong Kong’s market is its industry composition. The HKEX Main Boardis rooted in the ‘old’ economy that although has served the economy well, is extremely susceptible to external shocks and cyclical movements in the economy. Financial, and Property and Construction companies make up 44% of the Hong Kong stock exchanges’ total market capitalization, whereas only 10.2% is from IT companies as of the end of 2016.

While IT’s share of the market has increased from 3.76% in 2012 to its current level (14.3% YOY increase), it is still underrepresented compared to other major financial centres. For example, the market capitalization weighting and composition for the New York Stock Exchange (NYSE) is more balanced. Financial and Real Estate account for 35.9%, while Information Technology accounts for 33% of the S&P 500’s total market capitalization.

To address these problems, the Hong Kong Exchanges and Clearing (HKEX) issued two new concept papers last month. The first paper outlines plans to overhaul the current Growth Enterprise Market board (GEM) listing requirements, and second paper details a proposal of the “New Board” to attract “New Economy” companies.

Rough GEMs

GEM, first established in November 1999, originally addresses an issue that HK attracts too few SMEs, or ‘growth’ enterprises to list. It would allow companies ineligible to list on the Main Board to use the GEM as a “stepping stone” to the Main Board (streamline transfer process took effect on 1 July 2008). The higher listing requirements of the Main Board would originally have prevented these companies with potential from access to equity capital market financing.However, the current rules which allow these small, loosely regulated companies to list on GEM have created an environment where such problematic companies flourish. The NYSE, for example, says that companies trading at less than $1 per share (penny stocks) will face delisting after 30 consecutive days. HKEX has no such rules in place.

When 40% of the roughly 2000 common stocks traded is less than HK$1 per share, accounting for 4% of the total market capitalization of the exchange, it highlights the structural flaws created by GEM. New listings on GEM are only required to offer a minimum 25% of total shares to a minimum of 100 shareholders.

Since senior management is likely to keep the lion’s share for themselves, this creates a low liquidity, high volatility environment resulting from a high concentration of public shares in few shareholders. The potential big moves have attracted the attention of short sellers to descend on GEM-listed companies. In the recent stock rout, 7 of the 20 biggest decliners were listed on the GEM. The top three decliners were GEM companies: Luen Wong Group (-89%), Greater China Professional (-94%) and China Jicheng Holdings Ltd. (-95%).

Five Key Changes

The aforementioned first paper proposes to increase the listing requirements for GEM to tackle issues of low liquidity/high volatility and quality of listings. Some of the proposed changes include:- Increasing the minimum cash flow requirement from at least HK$20m to at least HK$30m: Greater cash flows indicate more operational stability to pay off short-term obligations

- Increasing the minimum market capitalization requirement from HK$100m to HK$150m: Higher market cap requirement reduces the number of potentially “bad” companies looking to obtain equity financing, increasing protection for public shareholders. Also, the higher market cap possibly represents greater confidence in the company

- Changing the post-IPO lock-up requirement on controlling shareholders from one year to two years: Longer lock-up period requirement would prevent controlling shareholders from trading on insider information, therefore increasing market confidence in the company

- Increasing the minimum public float value of issuing company securities from HK$30m to HK$45m: Greater public float value can increase market efficiency. However, it is necessary to increase the percentage share of public float (currently at 25%) to reduce share concentration

Addressing the New Economy

Another initiative proposed by HKEX is a new exchange platform for underrepresented “New Economy” sectors. The “New Economy” encompasses generally high-tech venture industries such as Biotech, Health Care Technology, Internet & Direct Marketing retail, Internet Software, IT Services, Software, Technology Hardware, Storage & Peripherals.Both the Main Board and GEM require that the company must be profitable to be considered for listing. Many of the “New Economy” sectors are unable to reach profitability due to factors including aggressive growth strategy and upfront research and development (R&D) costs. For example, biotech and healthcare tech companies have extremely high R&D costs, and would likely not be profitable until the product becomes commercially viable. HKEX seeks to address this missing market with the New board.

New board PRO companies need to have HK$200m minimum market capitalization and are only open to professional investors but do not require prior financial track record. Meanwhile, New Board PREMIUM companies need to have equivalent listing requirements as Main Board companies (minimum HK$500m market cap and public float of HK$125m) but are open to both retail and professional investors.

Furthermore, the New Boards would for the first time allow a weighted voting rights (WVR) structure which could make a listing in Hong Kong more attractive because it gives greater voting rights to founders, thus protect their vision for the company.

HKEX have explored the inclusion of WVR structures for SMEs in the GEM exchange back in 2014, after losing out on Alibaba’s IPO to NYSE because the HKEX refused to allow senior executives to nominate its board. However, the proposal was ultimately put on hold after mixed responses from over 200 respondents which consisted of large corporations, government and independent organisations. On the one hand, the ones who voted against WVR state that the structure violates the ‘one share, one vote’ principle of the HKEX.

On the other hand, the ones who voted for WVRs believed that it is applicable in certain circumstances, and the simplistic ‘one share, one vote’ principle can lead to short-termism in the absence of a controlling shareholder. No matter which side of the argument is correct, it is undeniable that Hong Kong’s loss is New York’s win. Alibaba went on to record the biggest ever IPO, raising over $25bn. Other developed markets have a similar, more flexible system in place for high tech, intangible asset-heavy companies.

For example, Snap Inc. has never made positive operating cash flow or profit, but still,manages to list on NYSE and was valued at US$25bn in this year’s hottest tech IPO. Co-Founders Evan Spiegel and Bobby Murphy hold a combined 88.5% of the voting power as a result of the triple-class WVR structure, giving them uncontested decision-making authority.

Keep up With the Competition

Major exchanges are developing innovative solutions to attract IPOs from foreign companies. Singapore stock exchange is actively considering the listing of companies with WVR structures, while the London Stock Exchange is considering an “international segment” on which large international companies with WVR structures can list.If HKEX does not take steps to keep up or go beyond the competition, they could get left behind in the modern financial system. The revisions to GEM could mitigate the issues resulting from the small public float, while the New Board can attract local “New Economy” sectors to consider Hong Kong over New York. Whether these changes will be effective or not, it is a step in the right direction.

Monday, January 7, 2019

Are Activist Investor's Market Manipulators? [Published on June 2017]

On March 24th, during a seemingly normal Friday in the Hong Kong stock market, chaos broke when Huishan Dairy’s share price plunged 85%, wiping out about $4.1bn in market value before the company stepped in to halt trading. There was no warning nor was there an immediate explanation for the sudden crash of one of the most stable stocks traded in Hong Kong.

However, in December last year, activist short seller Muddy Water published a two-part 60-page report announcing they were taking a short position in Huishan Dairy, accusing them of alleged numerous operating and accounting frauds and confidently stated their trademark phrase, “this stock is worth close to zero”.

Muddy Waters founder and CIO Carson Block first became famous in 2011 when its short sell report led to the bankruptcy of Toronto-listed Chinese company Sino-Forest. Since then, and now, traders take notice of tweets from himself or Muddy Waters, and whenever he appears on television because his comments can move markets.

Activist investors are those who have the resources and influence to have an impact on the direction of a company’s share price. High-profile hedge fund managers would often be activist investors, and they are almost always institutional investors.

Arguably the most famous activist investor is Bill Ackman, the Chief Executive Officer of Pershing Square Capital, a New York-listed hedge fund. Back in 2012, Ackman bet over $1bn on shorting sports nutrition company Herbalife, calling its multi-level marketing business model a pyramid scheme.

Herbalife and its billionaire majority shareholder Carl Icahn has vehemently denied Ackman’s claims on multiple occasions. This five-year saga still rages on today. Herbalife is currently winning as its stock price has risen nearly 40% since Ackman first attacked the company.

When investors short stocks, they borrow the stock from a broker to sell, then pay interest on the borrowing and any dividends the stock earns. Ackman is paying roughly $100m just to maintain his short position. In a June 2016 article, it states “[f]or Ackman to break even on his Herbalife short position, the hedge funder would have to see the stock to the low 30s.” One can expect the share price needs to be even lower now.

Carson Block visited Hong Kong to attend the Sohn conference on June 7th. The day before the conference, he paid a visit to Bloomberg’s office in Hong Kong and appeared on Bloomberg Markets: Asia. During the interview where he discussed topics on his short-selling research methodologies, Snap, and China’s economy, he explained that Chinese companies can manipulate their financial statements more easily and are, thus, more susceptible to fraudulent practices. When asked which company, he replied: “well you’ll have to find out tomorrow, but it will be Hong Kong-listed”.

The Hang Seng index fell after his comments, and some speculators began to short stocks that they thought would be named the following day. Some, including Andrew Clarke, director of trading at Mirabaud Asia, criticised Block for causing a panic sell-off in stocks that had no relation to his short target. Eventually, Block announced that Muddy Waters was shorting Man Wah, a Hong Kong-based manufacturer of furniture and household goods. Man Wah’s stock tumbled as much as 15% before ending the day 10.3% lower at HK$6.03 before the company’s shares are halted for trading. Man Wah has called those allegations “inaccurate” and “flawed” and has asked its lawyers to make a formal complaint to the Hong Kong securities regulator.

Carson Block and Bill Ackman are only two of the many activist investors out there. The question is: are their actions legal?

Market manipulation is a serious offense, and those liable would be fined heavily, banned, and/or prosecuted. Common activities that could be classified as market manipulation include creating a false impression of liquidity and artificially raising or lowering share prices and deliberately presenting false information leading to share price movements that benefit their own portfolio holdings. One is interested in the latter.

While activist investors are vocal and possibly harsh about their opinions, they do not make audacious claims without credible evidence. For example, Muddy Waters’ claim to fame comes from the fact that their research has produced quite a consistent track record, so it is difficult to argue that they produce false information. Also, with regards to Ackman vs. Herbalife, John Coffee, a securities law professor at Columbia University of New York, said "[w]hile Ackman is playing hardball with Herbalife, his actions aren’t illegal, and accusations of market manipulation would be overblown."

Although research is based on objective information, opinions are subjective. This is the reason why analyst ratings can be different for the same stock because it ultimately depends on the opinion of the analyst in question.

Most importantly, the market may not necessarily be swayed by a single investor’s opinion no matter how credible he/she is. In 2014, after Ackman’s three-hour presentation where he labeled then-Herbalife CEO Michael Johnson “a predator” and labeled the company “a criminal enterprise”, the market shrugged it off, and Herbalife’s stock rose over 20% the next day. Furthermore, Man Wah’s shares have increased to HK$7.22 (as of 16/06/2017), 52 cents above the price on the day Block announced shorting the company’s stock. Therefore, while activists have profited from their actions, it does not always produce favourable results because it ultimately hinges on whether they can convince the market to move in the direction they want.

However, in December last year, activist short seller Muddy Water published a two-part 60-page report announcing they were taking a short position in Huishan Dairy, accusing them of alleged numerous operating and accounting frauds and confidently stated their trademark phrase, “this stock is worth close to zero”.

Muddy Waters founder and CIO Carson Block first became famous in 2011 when its short sell report led to the bankruptcy of Toronto-listed Chinese company Sino-Forest. Since then, and now, traders take notice of tweets from himself or Muddy Waters, and whenever he appears on television because his comments can move markets.

What Are Activist Investors?

Activist investors are those who have the resources and influence to have an impact on the direction of a company’s share price. High-profile hedge fund managers would often be activist investors, and they are almost always institutional investors.

Arguably the most famous activist investor is Bill Ackman, the Chief Executive Officer of Pershing Square Capital, a New York-listed hedge fund. Back in 2012, Ackman bet over $1bn on shorting sports nutrition company Herbalife, calling its multi-level marketing business model a pyramid scheme.

Herbalife and its billionaire majority shareholder Carl Icahn has vehemently denied Ackman’s claims on multiple occasions. This five-year saga still rages on today. Herbalife is currently winning as its stock price has risen nearly 40% since Ackman first attacked the company.

When investors short stocks, they borrow the stock from a broker to sell, then pay interest on the borrowing and any dividends the stock earns. Ackman is paying roughly $100m just to maintain his short position. In a June 2016 article, it states “[f]or Ackman to break even on his Herbalife short position, the hedge funder would have to see the stock to the low 30s.” One can expect the share price needs to be even lower now.

Back to Muddy Waters…

Carson Block visited Hong Kong to attend the Sohn conference on June 7th. The day before the conference, he paid a visit to Bloomberg’s office in Hong Kong and appeared on Bloomberg Markets: Asia. During the interview where he discussed topics on his short-selling research methodologies, Snap, and China’s economy, he explained that Chinese companies can manipulate their financial statements more easily and are, thus, more susceptible to fraudulent practices. When asked which company, he replied: “well you’ll have to find out tomorrow, but it will be Hong Kong-listed”.

The Hang Seng index fell after his comments, and some speculators began to short stocks that they thought would be named the following day. Some, including Andrew Clarke, director of trading at Mirabaud Asia, criticised Block for causing a panic sell-off in stocks that had no relation to his short target. Eventually, Block announced that Muddy Waters was shorting Man Wah, a Hong Kong-based manufacturer of furniture and household goods. Man Wah’s stock tumbled as much as 15% before ending the day 10.3% lower at HK$6.03 before the company’s shares are halted for trading. Man Wah has called those allegations “inaccurate” and “flawed” and has asked its lawyers to make a formal complaint to the Hong Kong securities regulator.

Market Manipulators?

Carson Block and Bill Ackman are only two of the many activist investors out there. The question is: are their actions legal?

Market manipulation is a serious offense, and those liable would be fined heavily, banned, and/or prosecuted. Common activities that could be classified as market manipulation include creating a false impression of liquidity and artificially raising or lowering share prices and deliberately presenting false information leading to share price movements that benefit their own portfolio holdings. One is interested in the latter.

While activist investors are vocal and possibly harsh about their opinions, they do not make audacious claims without credible evidence. For example, Muddy Waters’ claim to fame comes from the fact that their research has produced quite a consistent track record, so it is difficult to argue that they produce false information. Also, with regards to Ackman vs. Herbalife, John Coffee, a securities law professor at Columbia University of New York, said "[w]hile Ackman is playing hardball with Herbalife, his actions aren’t illegal, and accusations of market manipulation would be overblown."

Although research is based on objective information, opinions are subjective. This is the reason why analyst ratings can be different for the same stock because it ultimately depends on the opinion of the analyst in question.

Actual Power

Most importantly, the market may not necessarily be swayed by a single investor’s opinion no matter how credible he/she is. In 2014, after Ackman’s three-hour presentation where he labeled then-Herbalife CEO Michael Johnson “a predator” and labeled the company “a criminal enterprise”, the market shrugged it off, and Herbalife’s stock rose over 20% the next day. Furthermore, Man Wah’s shares have increased to HK$7.22 (as of 16/06/2017), 52 cents above the price on the day Block announced shorting the company’s stock. Therefore, while activists have profited from their actions, it does not always produce favourable results because it ultimately hinges on whether they can convince the market to move in the direction they want.

*Update [08/01/2019]: Man Wah's stock has now fallen to HK$3.02 following continued weakness in the retail and furniture sector, proving Carson Block right all along.

Lastly, having activist investors can help improve the market’s efficiency. If and when fraud is detected, this would create pressure for other companies to improve their own practices to increase shareholder value. Also, it creates an incentive for the local stock exchange to tighten listing rules or conduct regular financial checks to give investors and prospective companies confidence to invest in and list on the exchange respectively. While the actions of activist investors may raise a few eyebrows, they can raise corporate governance standards to avoid targets in the future.

To conclude, the answer to the question is: yes, it is legal and may even be beneficial in the long run.

Lastly, having activist investors can help improve the market’s efficiency. If and when fraud is detected, this would create pressure for other companies to improve their own practices to increase shareholder value. Also, it creates an incentive for the local stock exchange to tighten listing rules or conduct regular financial checks to give investors and prospective companies confidence to invest in and list on the exchange respectively. While the actions of activist investors may raise a few eyebrows, they can raise corporate governance standards to avoid targets in the future.

To conclude, the answer to the question is: yes, it is legal and may even be beneficial in the long run.

The Hong Kong Housing Dilemma [Published on March 2017]

“Hong Kong” and “property prices”, more often than not, are uttered in the same sentence when talking about Asia’s financial hub.

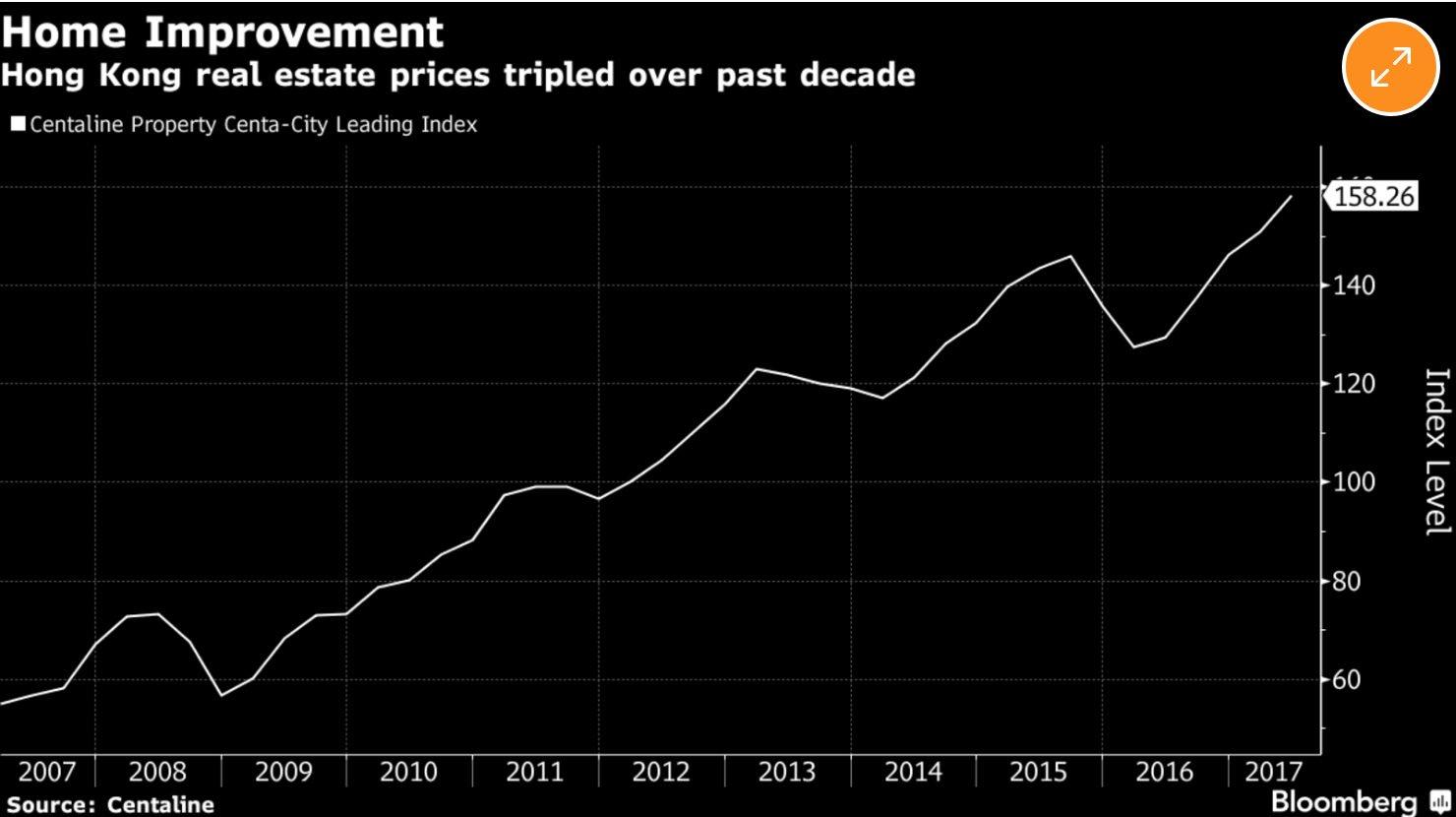

The former British colony’s housing market, while already recognised as the most unaffordable in the world for seven years in a row, continues to make record highs through the combination of investment from cash-rich mainland developers, low interest rates and a shortage of housing supply.

Earlier this year, two mainland Chinese companies outbid Hong Kong’s biggest developers for a waterfront site in Ap Lei Chau, a tiny island just south of HK island for a record HK$16.9bn (US$2.2bn).

According to Bloomberg’s estimates, it amounts to a price of HK$22100 per square foot. This is just the cost of the land – the selling price per square foot is almost certain to exceed HK$30000 when it goes to market.

HK housing prices are approaching their peak and economically unsustainable, said Cusson Leung, managing director at JP Morgan Chase & Co.’s Asia-Pacific equity research unit.

“Price increases have far outpaced GDP growth. Thus any external shocks could trigger tighter liquidity in the city’s banking system,” Leung says. Though the government has introduced measures to rein in the housing market by, for example, doubling the stamp duty tax from 8% to 15% for secondary and foreign home buyers in November last year, prices continued their upward march with no clear signs of slowing down in the near term.

Though the government has introduced measures to rein in the housing market, for example doubling the stamp duty tax from 8% to 15% for secondary and foreign home buyers in November last year, prices continued its upward march with no clear signs of slowing down in the near term.

Government policies are subject to enforcement and impact lag. These lags give people the opportunity to act before the new rules set in. When the Hong Kong government announced the increase in stamp duty, house prices went up rather than down because investors want to avoid paying taxes, which led to a sudden rush of demand to snap up properties before the tax hit them hard.

Hong Kong’s wealthy home buyers have found ways around these curbs and add to their already big portfolios. For example, purchasing multiple properties under one contract under their children’s name would qualify them as a first-time home buyer. Additionally, one can set up a foreign shell company that purchases the property and then buying the shell company that subjects them to only a 0.2% stamp duty since it is treated as a share transfer.

In fact, the number of first-time home buyers has increased from 30% to 70% after the tax was introduced. Since then, the government has closed the loophole such that purchasing multiple units with one contract at the same time would trigger the 15% stamp duty.

At the most basic level, housing is shelter: it is a place where one can safely sleep at night. But housing has transcended this simple definition to being an investment class that provides an alternative to equities and bonds.

People have different reasons for investing in housing. Some want to be landlords to rent out properties for a steady income; others may want to simply diversify their portfolio of assets away from traditional investment classes.

As such, housing has become an instrument for speculative investment. In Hong Kong, even public housing is not spared because existing public housing owners can sell their units on the secondary market, albeit with some conditions, where the price is ultimately tied to prevailing market prices for private housing.

The unaffordable housing adds to the growing discontent among the youth population in Hong Kong. Based on government data, there is at least a four-year waiting list for public housing units. The government has not been able to increase supply enough to offset demand, but more importantly, the idea of using housing to speculate increases in value needs to be changed.

If we assume the government can increase public housing supply free of political setbacks, one idea is to create separate markets between private and public housing. Under this idea, public housing units can only be resold at face value adjusted for core inflation, meaning that prices would not outpace real income, generating price stability and affordability.

Short to medium term remedies will need to contain an element which restricts speculative behaviour. Another idea is to increase the degree of illiquidity in the secondary home market, preventing speculative purchase and sale of properties.

For example, property buyers cannot list their properties for sale for at least ten years after the purchase date. This could also have an effect on the primary market because restricting flexibility in property transactions lowers the value of the property to investors because there is uncertainty on whether they can sell at the right time.

As astonishing as this may sound, much of Hong Kong’s land is undeveloped. Only 30% of HK’s total land area has been built on. In a recent interview on TVB Pearl’s ‘Straight Talk’ with host Michael Chugani, guest interviewee Mr. Shih Wing-ching, the founder and CEO of Centaline Property Agency, suggests that the government has a lot of spare land available. Developments using this land could enormously increase the supply of housing since residential buildings account for only 7% of Hong Kong’s land, of which 3% is public, and 4% is private.

There is strong economic interest for the HK government to not accelerate development because land and real estate is an important source of tax revenue. In FY2016-2017, the sum of stamp duties (10.8%) and premium from land sales (22.3%) accounted for nearly a third of government revenue for the year.

With the right policies, willingness of the government to use its resources, and consensus from the public, Hong Kong’s housing problems can be solved.

However, the messy state of Hong Kong politics has made progress difficult. Referring to Shih Wing-ching’s interview, he points to grim prospects that house prices will fall to a level such that ordinary citizens can afford to buy a property simply because the wealthy still demand property at current prices.

Unlike the previous housing supercycles of boom and bust such as those that followed the SARS outbreak in 2003 and the financial crisis in 2007, current prices look like they are going to stay for a while.

The former British colony’s housing market, while already recognised as the most unaffordable in the world for seven years in a row, continues to make record highs through the combination of investment from cash-rich mainland developers, low interest rates and a shortage of housing supply.

Earlier this year, two mainland Chinese companies outbid Hong Kong’s biggest developers for a waterfront site in Ap Lei Chau, a tiny island just south of HK island for a record HK$16.9bn (US$2.2bn).

According to Bloomberg’s estimates, it amounts to a price of HK$22100 per square foot. This is just the cost of the land – the selling price per square foot is almost certain to exceed HK$30000 when it goes to market.

Economically Unsustainable

HK housing prices are approaching their peak and economically unsustainable, said Cusson Leung, managing director at JP Morgan Chase & Co.’s Asia-Pacific equity research unit.

“Price increases have far outpaced GDP growth. Thus any external shocks could trigger tighter liquidity in the city’s banking system,” Leung says. Though the government has introduced measures to rein in the housing market by, for example, doubling the stamp duty tax from 8% to 15% for secondary and foreign home buyers in November last year, prices continued their upward march with no clear signs of slowing down in the near term.

Tax Evasion

Though the government has introduced measures to rein in the housing market, for example doubling the stamp duty tax from 8% to 15% for secondary and foreign home buyers in November last year, prices continued its upward march with no clear signs of slowing down in the near term.

Government policies are subject to enforcement and impact lag. These lags give people the opportunity to act before the new rules set in. When the Hong Kong government announced the increase in stamp duty, house prices went up rather than down because investors want to avoid paying taxes, which led to a sudden rush of demand to snap up properties before the tax hit them hard.

Hong Kong’s wealthy home buyers have found ways around these curbs and add to their already big portfolios. For example, purchasing multiple properties under one contract under their children’s name would qualify them as a first-time home buyer. Additionally, one can set up a foreign shell company that purchases the property and then buying the shell company that subjects them to only a 0.2% stamp duty since it is treated as a share transfer.

In fact, the number of first-time home buyers has increased from 30% to 70% after the tax was introduced. Since then, the government has closed the loophole such that purchasing multiple units with one contract at the same time would trigger the 15% stamp duty.

Evolution of Housing

At the most basic level, housing is shelter: it is a place where one can safely sleep at night. But housing has transcended this simple definition to being an investment class that provides an alternative to equities and bonds.

People have different reasons for investing in housing. Some want to be landlords to rent out properties for a steady income; others may want to simply diversify their portfolio of assets away from traditional investment classes.

As such, housing has become an instrument for speculative investment. In Hong Kong, even public housing is not spared because existing public housing owners can sell their units on the secondary market, albeit with some conditions, where the price is ultimately tied to prevailing market prices for private housing.

The unaffordable housing adds to the growing discontent among the youth population in Hong Kong. Based on government data, there is at least a four-year waiting list for public housing units. The government has not been able to increase supply enough to offset demand, but more importantly, the idea of using housing to speculate increases in value needs to be changed.

Solutions

If we assume the government can increase public housing supply free of political setbacks, one idea is to create separate markets between private and public housing. Under this idea, public housing units can only be resold at face value adjusted for core inflation, meaning that prices would not outpace real income, generating price stability and affordability.

Short to medium term remedies will need to contain an element which restricts speculative behaviour. Another idea is to increase the degree of illiquidity in the secondary home market, preventing speculative purchase and sale of properties.

For example, property buyers cannot list their properties for sale for at least ten years after the purchase date. This could also have an effect on the primary market because restricting flexibility in property transactions lowers the value of the property to investors because there is uncertainty on whether they can sell at the right time.

As astonishing as this may sound, much of Hong Kong’s land is undeveloped. Only 30% of HK’s total land area has been built on. In a recent interview on TVB Pearl’s ‘Straight Talk’ with host Michael Chugani, guest interviewee Mr. Shih Wing-ching, the founder and CEO of Centaline Property Agency, suggests that the government has a lot of spare land available. Developments using this land could enormously increase the supply of housing since residential buildings account for only 7% of Hong Kong’s land, of which 3% is public, and 4% is private.

There is strong economic interest for the HK government to not accelerate development because land and real estate is an important source of tax revenue. In FY2016-2017, the sum of stamp duties (10.8%) and premium from land sales (22.3%) accounted for nearly a third of government revenue for the year.

With the right policies, willingness of the government to use its resources, and consensus from the public, Hong Kong’s housing problems can be solved.

However, the messy state of Hong Kong politics has made progress difficult. Referring to Shih Wing-ching’s interview, he points to grim prospects that house prices will fall to a level such that ordinary citizens can afford to buy a property simply because the wealthy still demand property at current prices.

Unlike the previous housing supercycles of boom and bust such as those that followed the SARS outbreak in 2003 and the financial crisis in 2007, current prices look like they are going to stay for a while.

Hong Kong and Singapore: Battle of Giants [Published on January 2017]

Traditionally, Hong Kong and Singapore compete in many areas, including education and the quality of their trading ports. However, the cornerstone for (and subsequently a major area of) competition between both cities is their respective financial services sectors.

Despite their similarities, the development paths and comparative advantages of their respective financial centres are significantly different. While Hong Kong’s position as an international financial centre (IFC) was already established as early as the 1960s, as Singapore was just starting its first Asian currency market.

While Hong Kong remains unchallenged today in terms of Initial Public Offerings (IPOs) and mergers and acquisitions (M&A) activity (third overall, just behind London and New York, while Singapore lags in 19th place), Singapore’s rapid growth allowed it to dominate the region when it comes to commodities and foreign exchange trading.

This is not limited to competitiveness in the financial sector. In this years’ Global Competitiveness Index by the World Economic Forum, Hong Kong once again ranked below Singapore, the latter having come second and the former having dropped two places to ninth. Considering the components of this index further, the ‘Financial Market Development’ component also sees Singapore beating Hong Kong, albeit with a margin of 0.1 or 1.82%. While these rankings do not necessarily conclude which country is better, it serves as a good indicator of Hong Kong’s declining competitiveness in Asia as an IFC.

What makes a country or city an international financial centre? What makes IFCs is defined by many factors. They are notable for the competitiveness of their financial industries, highly-developed infrastructure and human capital, relatively unstrict regulatory environments, low taxes, and significant inward foreign direct investment.

For many years, Hong Kong’s international reputation comes from this cocktail that makes it an attractive destination for business. As evidence, many international firms set up their Asian headquarters in Hong Kong. It even has a skyscraper named the International Finance Centre in its financial district. But Singapore’s unprecedented growth sends warning signals that Hong Kong must improve or reinvent itself if it is to regain its throne as Asia’s financial lynchpin.

If there is an area in which Hong Kong has an absolute advantage over Singapore, it is its strong links and proximity to mainland China. Its growth story surpasses these two Asian dragons if one compares the extreme difficulty in managing a country of China’s size. Because of this, the Hong Kong Monetary Authority and Hong Kong Exchanges and Clearing have in the last two decades shifted the focus of their development strategies to China. Hong Kong is the world’s largest offshore renminbi exchange centre, taking up a staggering

Because of this, the Hong Kong Monetary Authority and Hong Kong Exchanges and Clearing have in the last two decades shifted the focus of their development strategies to China. Hong Kong is the world’s largest offshore renminbi exchange centre, taking up a staggering 70% of total transaction value for the Chinese currency.

Furthermore, as of October 31st, 2016, of the total number of listed companies on the Hong Kong stock exchange (1955) more than half (989) are based on the mainland. Strategic initiatives are known as the ‘Shanghai-HK Stock Connect’ and ‘Shenzhen-HK Stock Connect’, and have opened foreign investors into mainland-issued A-shares. Without China, Hong Kong would have at some point got stuck in a permanent economic slump.

Singapore is already feeling the strain, with the economy probably recording its “worst performance since the 2009 financial crisis". Both export-reliant, the two economies are vulnerable to external trade shocks, and higher US interest rates affecting capital flows into their respective economies. What is certain is that the title of Asia’s premier financial centre is up for grabs.

http://www3.weforum.org/docs/GCR2016-2017/05FullReport/TheGlobalCompetitivenessReport2016-2017_FINAL.pdf

http://www3.weforum.org/docs/gcr/2015-2016/Global_Competitiveness_Report_2015-2016.pdf

http://reports.weforum.org/global-competitiveness-report-2015-2016/competitiveness-rankings/#indicatorId=GCI.B.08

http://www.legco.gov.hk/research-publications/english/essentials-1516ise08-competitiveness-of-hong-kong-in-offshore-renminbi-business.htm

Grounded in Finance

Financial and insurance services (FIS) contributed approximately 24.5% of total services exports in Hong Kong in 2015. Meanwhile, FIS was one of the main drivers of 2015 real GDP growth in Singapore, contributing 0.7% to the total recorded figure of 2%. These figures highlight the economic importance of this sector to both economies.Despite their similarities, the development paths and comparative advantages of their respective financial centres are significantly different. While Hong Kong’s position as an international financial centre (IFC) was already established as early as the 1960s, as Singapore was just starting its first Asian currency market.

While Hong Kong remains unchallenged today in terms of Initial Public Offerings (IPOs) and mergers and acquisitions (M&A) activity (third overall, just behind London and New York, while Singapore lags in 19th place), Singapore’s rapid growth allowed it to dominate the region when it comes to commodities and foreign exchange trading.

Hot Competition

So how do they compare with each other? In the Global Financial Centres Index (GFCI) published by Z/Yen Group, which assesses the competitiveness of a country’s financial sector, Hong Kong ranked ahead of Singapore on sixteen out of twenty measures. But Singapore has overtaken Hong Kong to reach third place overall and remained in this position for the whole of 2016.This is not limited to competitiveness in the financial sector. In this years’ Global Competitiveness Index by the World Economic Forum, Hong Kong once again ranked below Singapore, the latter having come second and the former having dropped two places to ninth. Considering the components of this index further, the ‘Financial Market Development’ component also sees Singapore beating Hong Kong, albeit with a margin of 0.1 or 1.82%. While these rankings do not necessarily conclude which country is better, it serves as a good indicator of Hong Kong’s declining competitiveness in Asia as an IFC.

What makes a country or city an international financial centre? What makes IFCs is defined by many factors. They are notable for the competitiveness of their financial industries, highly-developed infrastructure and human capital, relatively unstrict regulatory environments, low taxes, and significant inward foreign direct investment.

For many years, Hong Kong’s international reputation comes from this cocktail that makes it an attractive destination for business. As evidence, many international firms set up their Asian headquarters in Hong Kong. It even has a skyscraper named the International Finance Centre in its financial district. But Singapore’s unprecedented growth sends warning signals that Hong Kong must improve or reinvent itself if it is to regain its throne as Asia’s financial lynchpin.

70% of RMB’s transaction value is Hong Kong-based

If there is an area in which Hong Kong has an absolute advantage over Singapore, it is its strong links and proximity to mainland China. Its growth story surpasses these two Asian dragons if one compares the extreme difficulty in managing a country of China’s size. Because of this, the Hong Kong Monetary Authority and Hong Kong Exchanges and Clearing have in the last two decades shifted the focus of their development strategies to China. Hong Kong is the world’s largest offshore renminbi exchange centre, taking up a staggering

Because of this, the Hong Kong Monetary Authority and Hong Kong Exchanges and Clearing have in the last two decades shifted the focus of their development strategies to China. Hong Kong is the world’s largest offshore renminbi exchange centre, taking up a staggering 70% of total transaction value for the Chinese currency.

Furthermore, as of October 31st, 2016, of the total number of listed companies on the Hong Kong stock exchange (1955) more than half (989) are based on the mainland. Strategic initiatives are known as the ‘Shanghai-HK Stock Connect’ and ‘Shenzhen-HK Stock Connect’, and have opened foreign investors into mainland-issued A-shares. Without China, Hong Kong would have at some point got stuck in a permanent economic slump.

A Title up for Grabs

It is possible that the new Trump-led US economy is likely to have significant effects on both Hong Kong and Singapore, due to the increasing uncertainty in emerging markets. China’s trade relationship with the US, amongst other things, could very well take a turn for the worse – leaving Hong Kong worse-off in the process.Singapore is already feeling the strain, with the economy probably recording its “worst performance since the 2009 financial crisis". Both export-reliant, the two economies are vulnerable to external trade shocks, and higher US interest rates affecting capital flows into their respective economies. What is certain is that the title of Asia’s premier financial centre is up for grabs.

Sources:

https://www.mti.gov.sg/ResearchRoom/SiteAssets/Pages/Economic-Survey-of-Singapore-2015/FullReport_AES2015.pdf http://www3.weforum.org/docs/GCR2016-2017/05FullReport/TheGlobalCompetitivenessReport2016-2017_FINAL.pdf

http://www3.weforum.org/docs/gcr/2015-2016/Global_Competitiveness_Report_2015-2016.pdf

http://reports.weforum.org/global-competitiveness-report-2015-2016/competitiveness-rankings/#indicatorId=GCI.B.08

Sunday, January 6, 2019

Why Central Banks Should Surprise Markets [Published on July 2016]

Volatile financial markets, which is a by-product of uncertainty in fundamental signals in economics or politics, offer investors a rare opportunity to earn big money. However, the migration to what investors regard as ‘safe haven’ assets shed light on the risk-averse investment behaviors, especially due to the risks from ‘Brexit’ and the rise of Republican Nominee Donald Trump recently. For example, in the months leading up to and on the day of the ‘Brexit’ vote, the Japanese Yen outperformed against all other major currencies, and Gold has surged over 22% since January.

Long story short, volatility is not good in the eyes of policymakers. It makes investors cautious about risky assets (i.e. stocks) which reduce business investment, GDP growth, and wage growth. Central banks have traditionally played the role of leading and stabilizing markets through the use of Forward Guidance, a key Central Bank policy tool to announce the expected path of interest rate to traders and investors.

If you have read my previous article here, I argued that the advancements in the financial markets over time have partially displaced power from policymakers to investors. Large amounts of information have fundamentally changed investors’ behaviors from merely being responsive to speculative in the markets. Speculation involves making predictions; forward-looking investors make their investments today in anticipation of a favorable situation to which they could profit from in the future. The danger of speculation is that it could become manipulation; in effect, the market dictates the action of policymakers because any significant decision must be carefully evaluated against the economic indicators, and that includes signals from the markets.

Let us travel back in time to January 2016, during the first Federal Open Market Committee (FOMC) meeting. The US economy started the year strongly, with consumer spending, wages and inflation picking up from the previous quarter, suggesting the economy is robust enough to endure a planned rate hike in June. Flash forward several months to May, the bond market issues an ominous warning by a flattening of the yield curve depicted by the shrinking gap in yield between the 2-year and 10-year Treasury bonds in the graph below:

The flattening of the yield curve often coincides with a recession, however, economists were not worried about the impact on the U.S. economy, but the world economy. The market predicted that a rate hike in June would have a negative impact on world economies enduring sluggish growth and uncertain political landscapes, and priced the market accordingly. In the end, the Federal Reserve refrained from raising rates. Here are the two extracts from the Wall Street Journal that elaborates on this:

- Favourable 2016 economic data - http://www.wsj.com/articles/u-s-growth-revised-higher-in-fourth-quarter-1456493673

- Flattening yield curve - http://blogs.wsj.com/moneybeat/2016/05/24/signals-from-the-u-s-yield-curve-world-cant-handle-fed-rate-hikes/

Here is an interesting method: what if Central Banks were to intentionally surprise markets?

It is certainly a controversial idea, but it is not completely irrational. An element of unpredictability is necessary when markets need to be corrected to achieve policy targets. Compared to QE and negative interest rates, this is about as unconventional as it gets for Central Bank policy. We will do a case study on the Bank of Japan (BOJ) and the Yen. Below is a 5-year chart of the USDJPY (2011 - 2016):

One of the policies that Prime Minister Shinzo Abe advocated is monetary stimulus; under economic theory, the stimulus would make it cheaper to borrow, increase consumption and inflation, and depreciate the yen to make exports more competitive. When BOJ governor Haruhiko Kuroda took office in March 2013, he immediately surprised by announcing his plan to increase the monthly bond purchase program to 7.5 trillion yen and double the monetary base. Because the stimulus was greater than expected, markets took the news positively Yen depreciated very sharply by 8 percent, and continued to depreciate with speculation of further stimulus. This was a minor success in prime minister Abe’s economic goals to fuel export competitiveness.

However, three years of underwhelming economic data have changed the market’s mind, thereby signaling the Yen to reverse its downtrend. The Yen’s appreciation is exacerbated by its safe haven from the aforementioned risks. Kuroda surprised again at the beginning of 2016 by setting the benchmark interest rate to minus 0.1%. This time, the Yen fell on the announcement, but it did little to re-instill confidence in the BOJ’s easing policies to arrest deflation as it kept its asset purchase program unchanged. In this scenario, the aggregate effect did not exceed expectations and therefore did not alter the markets’ overall sentiment.

For Central Banks to influence markets it has to exceed market expectations through a ‘positive’ surprise. This particular case in the BOJ can be applied to the European Central Bank (ECB) when it cut rates and expanded QE in March 2016. Initially, the Euro fell over 1.6% against the US Dollar on the announcement but rebounded to end the day 0.6% higher after prospects of further stimulus is cut short.

One might sympathize with the Central Banks because it has been a scapegoat for scrutiny by investors that feel they betrayed their expectations to offer more stimulus. It also does not help when they continue to be at the center of attention because of QE and negative interest rate experiments. Clearly, the Central Bank cannot go at it alone; effective policy requires a simultaneous input from both fiscal and monetary tools. The coordination of both sets of tools has been disappointing. Mr. Mohammed El-Erian, the former CEO of PIMCO and a Bloomberg View Columnist, has continually expressed that well-constructed fiscal policy and structural reforms have been lacking.

Ultimately, the decision on whether to calm or jolt the market is hugely dependent on the macroeconomic effects that policymakers desire. The ideal weapon is coordinating fiscal and monetary policy together to convey a strong and confident message to the markets, but this is not always possible because of the ‘implementation lag’ between both tools. In light of this, the Central Bank should have the courage to occasionally remind the market that it is still a force to be reckoned with in an era where the effects of monetary policy are straying away from the forces of economics.

Sources:

http://www.bloomberg.com/news/articles/2013-04-04/bank-of-japan-boosts-bond-purchases-at-kuroda-s-first-meeting

http://www.bloomberg.com/news/articles/2016-03-10/ecb-cuts-all-rates-as-qe-boosted-to-80-billion-euros-a-month

Subscribe to:

Comments (Atom)