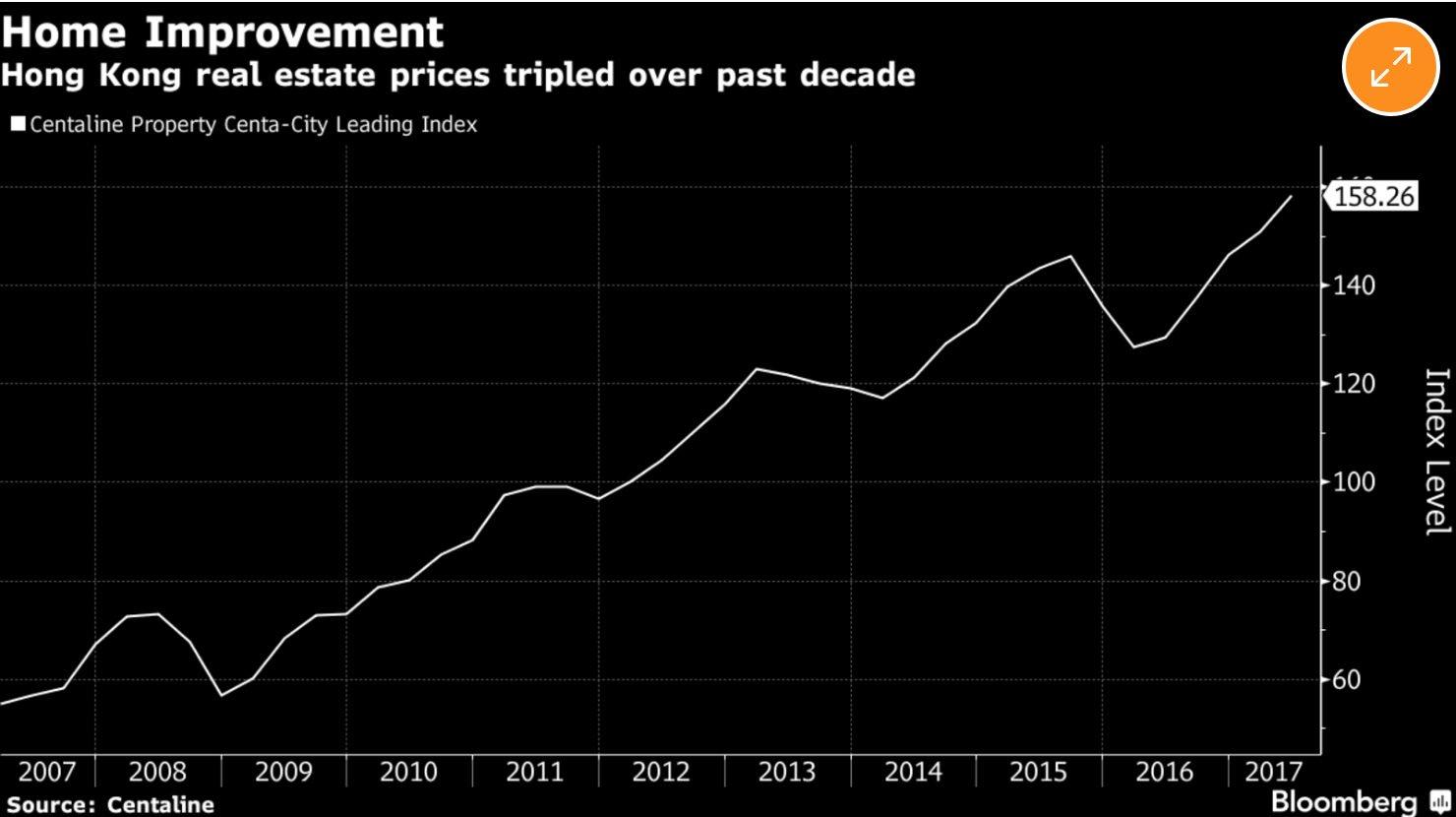

The former British colony’s housing market, while already recognised as the most unaffordable in the world for seven years in a row, continues to make record highs through the combination of investment from cash-rich mainland developers, low interest rates and a shortage of housing supply.

Earlier this year, two mainland Chinese companies outbid Hong Kong’s biggest developers for a waterfront site in Ap Lei Chau, a tiny island just south of HK island for a record HK$16.9bn (US$2.2bn).

According to Bloomberg’s estimates, it amounts to a price of HK$22100 per square foot. This is just the cost of the land – the selling price per square foot is almost certain to exceed HK$30000 when it goes to market.

Economically Unsustainable

HK housing prices are approaching their peak and economically unsustainable, said Cusson Leung, managing director at JP Morgan Chase & Co.’s Asia-Pacific equity research unit.

“Price increases have far outpaced GDP growth. Thus any external shocks could trigger tighter liquidity in the city’s banking system,” Leung says. Though the government has introduced measures to rein in the housing market by, for example, doubling the stamp duty tax from 8% to 15% for secondary and foreign home buyers in November last year, prices continued their upward march with no clear signs of slowing down in the near term.

Tax Evasion

Though the government has introduced measures to rein in the housing market, for example doubling the stamp duty tax from 8% to 15% for secondary and foreign home buyers in November last year, prices continued its upward march with no clear signs of slowing down in the near term.

Government policies are subject to enforcement and impact lag. These lags give people the opportunity to act before the new rules set in. When the Hong Kong government announced the increase in stamp duty, house prices went up rather than down because investors want to avoid paying taxes, which led to a sudden rush of demand to snap up properties before the tax hit them hard.

Hong Kong’s wealthy home buyers have found ways around these curbs and add to their already big portfolios. For example, purchasing multiple properties under one contract under their children’s name would qualify them as a first-time home buyer. Additionally, one can set up a foreign shell company that purchases the property and then buying the shell company that subjects them to only a 0.2% stamp duty since it is treated as a share transfer.

In fact, the number of first-time home buyers has increased from 30% to 70% after the tax was introduced. Since then, the government has closed the loophole such that purchasing multiple units with one contract at the same time would trigger the 15% stamp duty.

Evolution of Housing

At the most basic level, housing is shelter: it is a place where one can safely sleep at night. But housing has transcended this simple definition to being an investment class that provides an alternative to equities and bonds.

People have different reasons for investing in housing. Some want to be landlords to rent out properties for a steady income; others may want to simply diversify their portfolio of assets away from traditional investment classes.

As such, housing has become an instrument for speculative investment. In Hong Kong, even public housing is not spared because existing public housing owners can sell their units on the secondary market, albeit with some conditions, where the price is ultimately tied to prevailing market prices for private housing.

The unaffordable housing adds to the growing discontent among the youth population in Hong Kong. Based on government data, there is at least a four-year waiting list for public housing units. The government has not been able to increase supply enough to offset demand, but more importantly, the idea of using housing to speculate increases in value needs to be changed.

Solutions

If we assume the government can increase public housing supply free of political setbacks, one idea is to create separate markets between private and public housing. Under this idea, public housing units can only be resold at face value adjusted for core inflation, meaning that prices would not outpace real income, generating price stability and affordability.

Short to medium term remedies will need to contain an element which restricts speculative behaviour. Another idea is to increase the degree of illiquidity in the secondary home market, preventing speculative purchase and sale of properties.

For example, property buyers cannot list their properties for sale for at least ten years after the purchase date. This could also have an effect on the primary market because restricting flexibility in property transactions lowers the value of the property to investors because there is uncertainty on whether they can sell at the right time.

As astonishing as this may sound, much of Hong Kong’s land is undeveloped. Only 30% of HK’s total land area has been built on. In a recent interview on TVB Pearl’s ‘Straight Talk’ with host Michael Chugani, guest interviewee Mr. Shih Wing-ching, the founder and CEO of Centaline Property Agency, suggests that the government has a lot of spare land available. Developments using this land could enormously increase the supply of housing since residential buildings account for only 7% of Hong Kong’s land, of which 3% is public, and 4% is private.

There is strong economic interest for the HK government to not accelerate development because land and real estate is an important source of tax revenue. In FY2016-2017, the sum of stamp duties (10.8%) and premium from land sales (22.3%) accounted for nearly a third of government revenue for the year.

With the right policies, willingness of the government to use its resources, and consensus from the public, Hong Kong’s housing problems can be solved.

However, the messy state of Hong Kong politics has made progress difficult. Referring to Shih Wing-ching’s interview, he points to grim prospects that house prices will fall to a level such that ordinary citizens can afford to buy a property simply because the wealthy still demand property at current prices.

Unlike the previous housing supercycles of boom and bust such as those that followed the SARS outbreak in 2003 and the financial crisis in 2007, current prices look like they are going to stay for a while.

Valuable info. Lucky me I found your web site by accident, and I'm shocked why this accident did not happened earlier! I bookmarked it. a level economics online tutor

ReplyDeleteYou can definitely see your expertise in the work you write. The world hopes for even more passionate writers like you who are not afraid to say how they believe. Always follow your heart.economics tuition

ReplyDelete